Location: Home >> Detail

J Sustain Res. 2025;7(4):e250063. https://doi.org/10.20900/jsr20250063

,

Boyoung Kim *

,

Boyoung Kim *

Seoul Business School, aSSIST University, Seoul 03767, Korea

* Correspondence: Boyoung Kim

As Environmental, Social, and Governance (ESG) principles become increasingly integrated into corporate strategy and operations, many countries have implemented tax benefits to encourage companies to engage in ESG-oriented initiatives. Therefore, it is essential to manage tax benefits in parallel with ESG practices. This study aims to empirically assess the effect of corporate ESG management on tax benefits, and both financial and non-financial corporate performance through the mediating factor of tax benefits. ESG management is divided into three components—ESG—which are set as independent variables. Tax benefits are treated as a mediating variable, while financial and non-financial performance are used as dependent variables. The research model was constructed and hypotheses were formulated for structural equation analysis. A total of 262 questionnaires were collected and analyzed from tax leaders in large South Korean companies. The analysis showed that ESG components—environmental, social contribution, and governance—had a positive effect not only tax benefits but also both financial and non-financial corporate performance. The governance factor had the most significant impact on tax benefits, which were shown to have a stronger positive effect on non-financial performance than financial performance. These results confirm that companies implementing ESG strategies to enhance corporate performance should prioritize reinforcing ESG related tax benefit initiatives within their finance and tax teams.

The importance of corporate social responsibility is being emphasized for sustainable development, and many financial institutions around the world are using ESG evaluation data to evaluate companies [1]. ESG management is considered an important factor, especially when investors make decisions, along with financial indicators from a social responsibility investment (SRI) or sustainable investment (SI) perspective [2–4]. Companies make decisions by integrating non-financial factors, such as ESG management, which does not rely solely on financial performance but significantly affects future corporate value and sustainability from a long-term perspective [5–7]. Many previous studies have shown that ESG practices have a positive impact on corporate performance [8–13]. ESG activities have a positive impact on the corporate environment and workforce, increasing the likelihood of sound investment decisions. Research has shown that ESG participation is associated with more stable corporate governance, greater interest in the environment, and sustainable development issues, reduced profit volatility, and cost savings [14].

Accordingly, many governments around the world are actively discussing how to provide tax benefits to companies based on ESG evaluation to increase their sustainability and foster globally competitive companies [15]. In South Korea, companies listed on the Korea Exchange (KRX) with assets exceeding KRW 2 trillion will be required to disclose their ESG management reports starting in the 2025s, and ESG-related tax benefit policies and guidelines are being published and implemented to cope with the evolving regulatory framework [16]. As a result, changes in corporate tax rates according to ESG ratings are strengthening the strategic integration of ESG management and tax plans. Companies seeking to improve their performance through ESG-oriented management can enjoy various strategic benefits. Therefore, preferential tax benefits play a pivotal role in encouraging voluntary and active ESG performance enhancement [17].

McGuire et al. [18] emphasized that ESG management activities such as environmental protection, social contribution, and ethical governance have a significant impact on tax strategies as well as corporate business strategies. The related studies have focused on ESG activities and tax avoidance. Davis et al., [19] argued that there is a possibility of performing tax avoidance for the purpose of raising additional funds consumed by ESG activities. In response, Sadjiarto et al. [20] demonstrated the relationship that socially responsible companies are negative for aggressive tax avoidance. Bresan [21] and Mitrolia et al. [22] also verified that disclosure of sustainable management affects aggressive tax avoidance, and that companies that are passive about sustainable management tend to avoid aggressive taxes.

However, as Lanis and Richardson [23] argued, companies may be passive in tax avoidance due to concerns about the damage to the corporate reputation that will occur when tax evasion is detected, and the motivation for tax avoidance is reduced as the government provides various tax benefits related to ESG to promote corporate ESG management. In addition, Ma and Park [24] argued that if the government strengthens the ESG activity tax benefit strategy for companies, companies are more likely to strengthen sustainable management activities such as ESG practices rather than focusing on minimizing taxes in the short term. Furthermore, Atanasasov and Liu [25] explain that ESG tax benefits act as an important mechanism to ease financial constraints on companies, expand capital acquisition channels, and ease financing risks associated with implementing ESG-oriented corporate governance practices.

As such, most studies have argued that tax benefits have a positive effect on promoting ESG management activities of companies [26–28]. However, as Zhang et al. [29] augured, the studies that empirically verify this relationship are still insufficient. Therefore, this study aims to examine whether a company’s ESG management is directly related to tax benefits and verifies the impact of tax benefits on financial and non-financial corporate performance. The study finally contributes to strengthening tax incentives for ESG management and increasing the interest of tax experts within the company through empirical verification that ESG activities positively impact corporate performance through tax incentives.

In these backgrounds this study is organized as follows: Section 2 explains the relationship between ESG management, tax benefits, and corporate performance, and establishes research hypotheses based on them. Section 3 proposes research models, survey designs, and data collection and analysis methods. Section 4 mentions hypothesis verification results. Section 5 describes the main issues derived from the analysis. Finally, Section 6 provides academic implications and practical insights for improving corporate ESG-related tax benefits and ESG activities led by tax management leaders.

Tax benefits are economic benefits that apply to specific accounts or investments that receive tax breaks, tax deferrals, or tax exemptions under laws and regulations. Tax benefits refer to incentives provided through corporate tax laws for a company’s production, management, investment, and financial activities [17]. The first approach involves pre-tax profit deductions, which refer to legitimate expenses incurred in generating actual income. This includes costs, operating expenses, taxes, losses, and other expenses of goods sold and is allowed as a deduction when calculating taxable income. The second approach includes tax incentives such as desirable tax rates, gross income deductions, additional deductions for certain types of expenses, accelerated depreciation through asset value growth, and deductions for deferred tax liabilities [30,31]. The government provides various tax incentives to support business growth and promote specific industries. Tax incentives can be broadly classified into short-term and long-term benefits. Short-term tax incentives can result in deferred tax liabilities by minimizing the tax burden during the taxable period. This includes short-term income tax exemptions or tax credits [32], and long-term tax incentives include long-term income tax exemptions or tax credits [33].

ESG tax benefits are tax breaks or deductions provided by the government to encourage business ESG management activities. ESG tax benefits refer to governments deducting or exempting certain tax liabilities for reasons related to achieving specific policy goals or tax administration or technical considerations [17]. They also refer to deducting or exempting certain tax liabilities granted by the state to corporate taxpayers as a policy tool to promote ESG management. A company’s ESG management is not only a means of enhancing its reputation, but it is also used as an effective strategy for tax incentives and minimizing the risk of tax compliance. Furthermore, Lower tax burdens can improve operating cash flows, allowing companies to autonomously invest in R&D and new businesses without relying on internal or external financing, contributing to strengthening long-term sustainable growth. Strong ESG management companies can gain higher social trust, securing funds from investors and financial institutions at lower interest rates or on more favorable terms, minimizing capital costs. Visible tax benefits lead to tangible income, leading to higher equity market premiums and higher corporate value, contributing to lower weighted average capital costs [34].

Garcia-Bernando et al. [28] empirically investigated the impact of corporate ESG practices on tax avoidance, and found that higher ESG participation was significantly associated with lower levels of corporate tax avoidance. Bresan [21] explained that the social aspect has an important impact on reducing tax avoidance among ESG factors. Allen et al. [26] and Chen & Lin [27] also found that foreign investors tend to invest more in companies with high ESG ratings and significant tax benefits. Zhang et al. [29] found that in terms of environmental factors and tax benefits, environmental and green taxes play an increasingly important role in responding to climate change and regulating the national economy through the promotion of green production and consumption.

In response, Milne [35] explains through research the importance of a policy transition from a traditional approach that uses income collected from environmental taxes to funding infrastructure and services for environmental protection to providing tax benefits to promote environmentally friendly activities. In addition, Wahyunita et al. [36] explained that providing benefits in line with more comprehensive social values in terms of corporate tax will strengthen corporate ethical and social value activities. Prasetyo and Arif [37] emphasized the importance of securing incentive mechanisms within corporate tax strategies to sustain ethical tax practices in corporate activities. Consequently, these prior studies allow companies to consider positive synergies when corporate social and ethical activities are strengthened and linked to tax benefits in addition to financial performance through ESG activities.

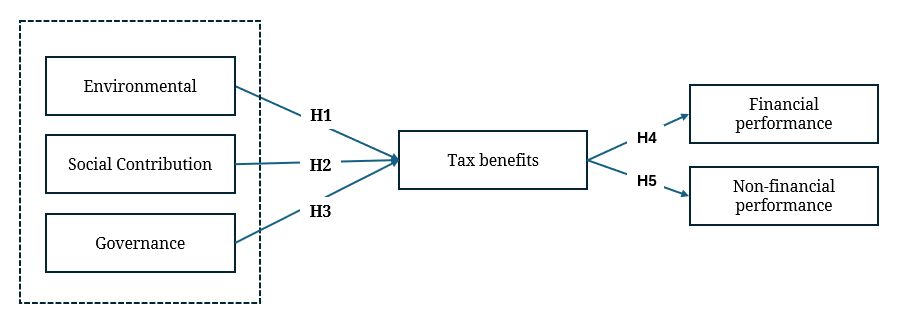

Hypothesis 1 (H1). Environment(E) among corporate ESG management activities will have a positive (+) effect on tax benefits.

Hypothesis 2 (H2). Social(S) among corporate ESG management activities will have a positive (+) effect on tax benefits.

Hypothesis 3 (H3). Governance(G) among corporate ESG management activities will have a positive (+) effect on tax benefits.

Tax Benefits and Corporate PerformanceAccording to Zwick and Mahon [38], companies can minimize tax costs through tax avoidance, which reduces outgoing cash flow and ultimately has a positive impact on corporate value. Eichfelder et al. [39] analyzed the relationship between tax benefits and revenue management and found that higher tax benefits companies are more likely to adopt aggressive tax strategies that leverage discretionary accruals to further minimize reported returns. Blaylock et al. [40] demonstrated that management participated in revenue management due to tax benefits or tax burdens, resulting in a decrease in the quality of accruals. Fan and Liu [41] demonstrated the effectiveness of tax benefits through tax incentive programs in terms of their impact on investment and demonstrated that tax benefits are directly utilized for investment. Wang et al. [42] reported that when companies receive tax benefits, management is less pressured about net income, resulting in improved quality of accounting information.

Tax incentives for ESG management activities have a direct impact on a company’s financial and non-financial performance [43]. Studies have shown that Bøler et al. [44] argued that a tax credit policy for ESG management effectively improves a company’s resilience to risk. In addition, many preceding studies explain that tax incentives for ESG management have a positive effect on improving corporate investment and productivity. In the end, as Dada et al. [45] and McGuire et al. [18] argued, ESG tax incentives can have a positive impact on strengthening corporate competitiveness and improving corporate performance in many ways.

Furthermore, from a non-financial perspective, tax benefits can create long-term stakeholder value and impact non-financial performance such as organizational trust, customer satisfaction, and internal collaboration [45]. Tax incentives through ESG activities can have a significant long-term impact on corporate sustainability. ESG-related tax incentives enable companies to exercise social responsibility, earning the trust of customers and employees, which increases customer loyalty and reduces employee turnover [46]. They can also play an important role in enhancing a company’s brand image and reputation [47]. In particular, corporations that maintain transparent governance enhance trust among investors and other stakeholders [48] and practice ethical management, thereby creating an environment in which investors are willing to invest with long-term confidence [49]. In this regard, tax benefits contribute not only to short-term profitability but also to the establishment of a sustainable business model that enhances long-term corporate value.

Thus, tax benefits are expected to have a positive impact not only on financial performance such as increased revenue, cost deduction, and lower cost of capital but also on non-financial performance including employee satisfaction, customer satisfaction, improvement of organizational culture, and enhanced corporate reputation. In light of these findings, this study formulated the following hypothesis.

Hypothesis 4 (H4). Tax benefits will have a positive (+) effect on a corporation's financial performance.

Hypothesis 5 (H5). Tax benefits will have a positive (+) effect on a corporation's non-financial performance.

This study empirically analyzes the impact of ESG management on tax benefits and corporate performance. To this end, a research model was designed as shown in Figure 1 in consideration of structural equation modeling (SEM) based on the structural equation model. The independent variables of the model were designed as ESG management factors such as environmental, social contribution, and governance. The dependent variable is the financial and non-financial performance of the company. Tax benefits were used as mediating variable.

Figure 1. Research model.

Figure 1. Research model.

In this study, ‘environment’ means the various eco-friendly corporate activities with the aim of improving performance. ‘Society’ refers to corporate social responsibility activities for guaranteeing labor rights, promoting gender equality, providing a safe working environment, contributing to local communities, and protecting human rights. ‘Governance’ refers to establishing and maintaining a fair and transparent corporate governance system by emphasizing transparency and accountability in management decision-making processes. ‘Tax benefit’ refers to various preferential tax measures provided by the government to minimize the tax burden on certain taxpayers, whether individual or corporate. ‘Corporate performance’ refers to financial performance such as growth and profitability, and non-financial performance such as corporate reputation, trust, and market competitiveness.

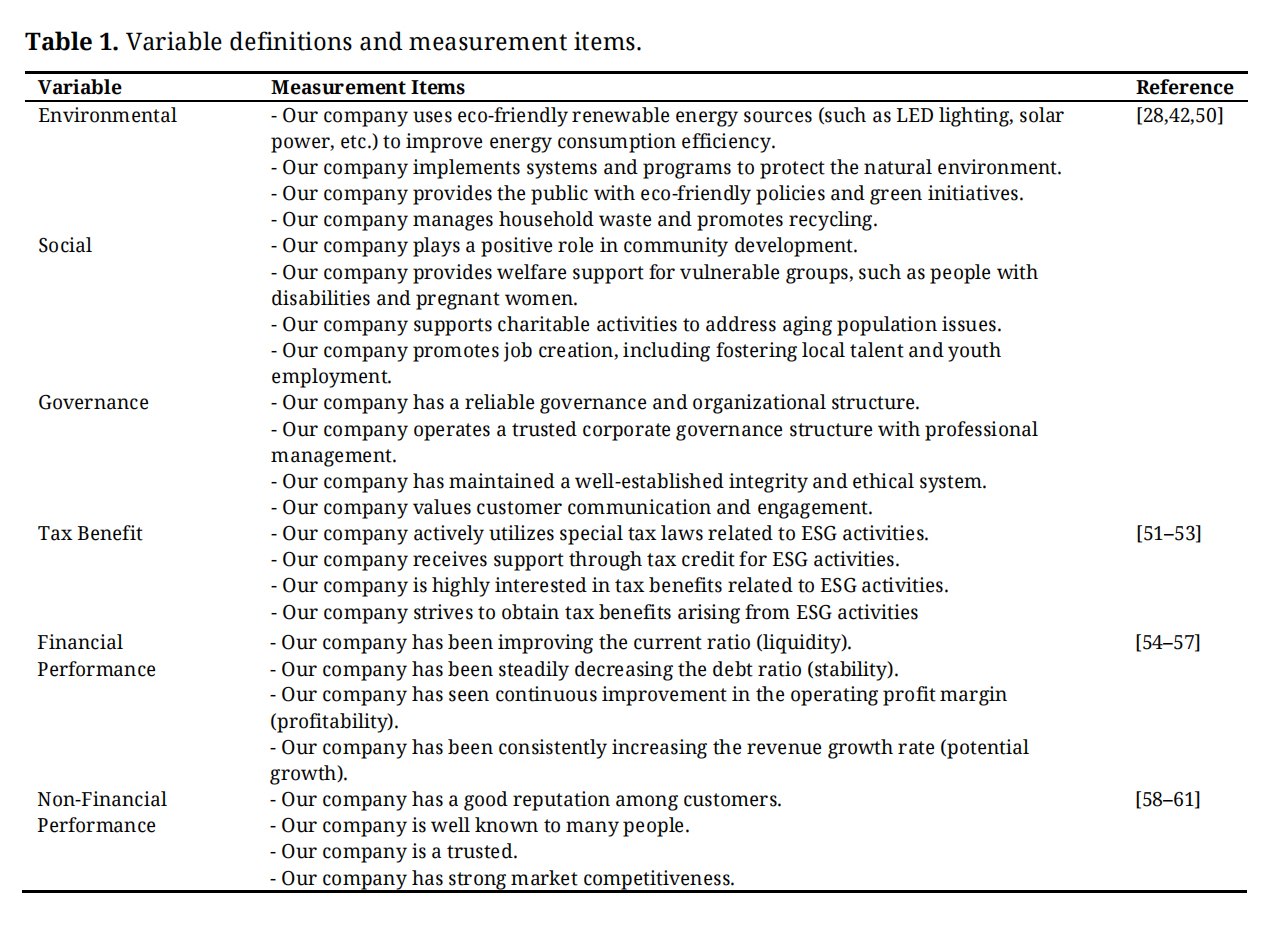

As shown in Table 1, the defined variables consisted of a total of 24 questionnaires based on previous studies. It is reported that about 17,000 certified tax accountants work in manufacturing, service, and IT industries located in the Seoul metropolitan area in South Korea. This study randomly surveyed a total of 300 responses to these samples. Data collection was conducted through an online survey over a three-week period from August 13 to September 3, 2024. Finally, the unfaithful responses were removed and a total of 262 valid samples were analyzed. SPSS 22.0 (IBM Korea, Seoul, South Korea) was used for demographic characteristics and descriptive statistics analysis and exploratory factor analysis. For path analysis of hypotheses, structural equation model, model verification, and path analysis were used AMOS 21.0 (IBM Korea, Seoul, South Korea).

Table 1. Variable definitions and measurement items.

Table 1. Variable definitions and measurement items.

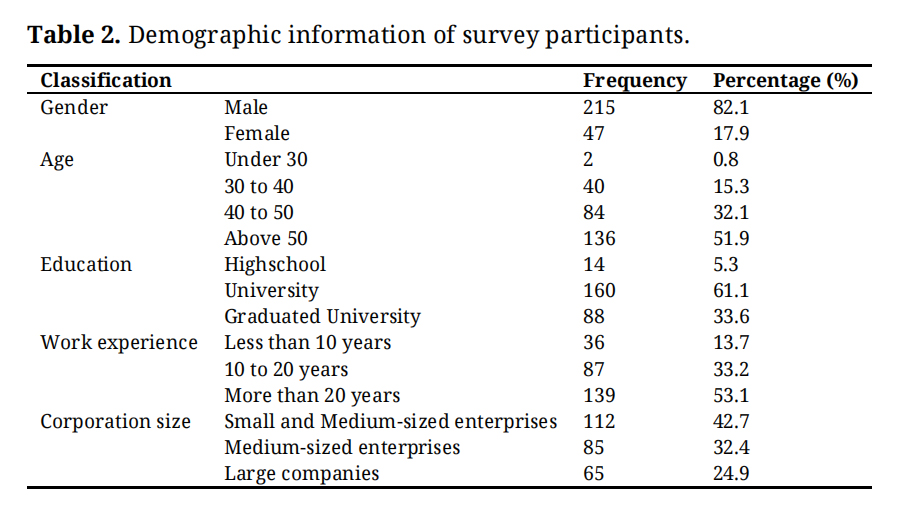

At the characteristics of the analysis data sample as shown in Table 2, 82.1% of the participants were male and 17.9% were female. In terms of age, 51.9% were over 50 years of age, 32.1% were in their 40s, 15.3% were in their 30s, and 0.8% were under 30s. In terms of educational background, 61.1% of people had a bachelor's degree and 33.6% were from college. In terms of career, 53.1% had more than 20 years of experience, 33.2% were under 10 to 20 years of experience, and 13.7% were under 10 years of experience. As for the size of the company, 42.7% of the respondents were employed in small and medium-sized companies, 32.4% were in mid-sized companies, and 24.8% were in large companies.

Table 2. Demographic information of survey participants.

Table 2. Demographic information of survey participants.

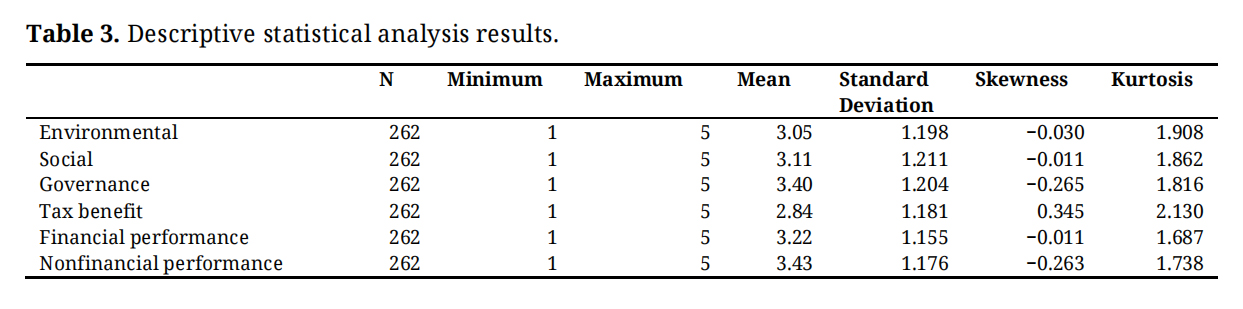

Descriptive statistical analysis of variables was conducted (see Table 3). First, the average of the ESG environment was found to be 3.05 with a standard deviation of 1.198. The average of ESG social contribution was found to be 3.11 with a standard deviation of 1.211. The average of ESG governance was found to be 3.40 with a standard deviation of 1.204. The average of tax incentives was found to be 2.84 with a standard deviation of 1.181. The average of financial corporate performance was found to be 1.155. The average of non-financial corporate performance was found to be 3.43 with a standard deviation of 1.176. Skewness and kurtosis were used to confirm the normality of the data. As a result of the analysis, it was analyzed that the univariate normality assumption, in which skewness never exceeded 3 and kurtosis never exceeded 8, was valid.

Table 3. Descriptive statistical analysis results.

Table 3. Descriptive statistical analysis results.

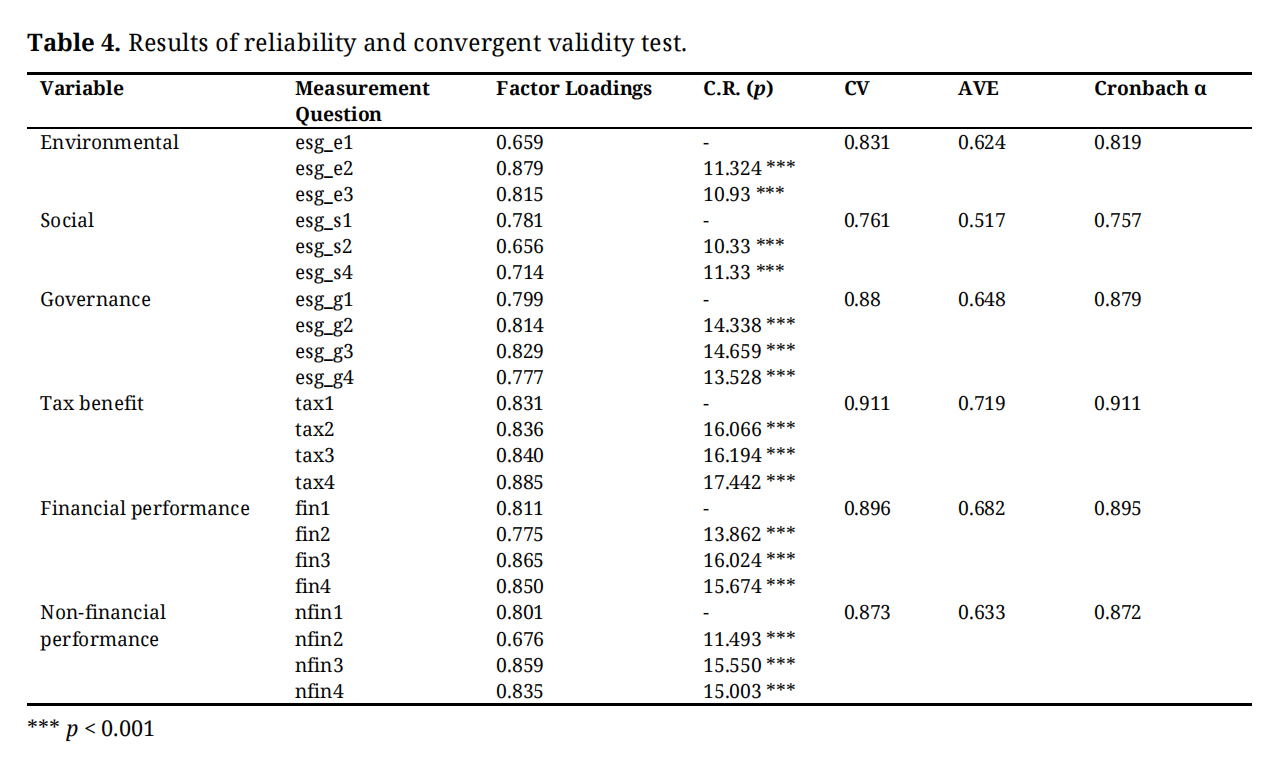

For exploratory factor analysis, as shown in Table 4, the factor rotation, Kaiser-Meier-Olkin (KMO) test, and Bartlett’s sphericity test were performed simultaneously using the orthogonal rotation method. The KMO scale of sampling adequacy was 0.94, showing an appropriate level of fitness, and Bartlett’s sphericity test showed a value of less than 0.001, confirming the appropriateness of factor analysis. Factor loading values were good, ranging from 0.656 to 0.885 (all above 0.6), and construct validity (CV) was significant, ranging from 0.831 to 0.911. The mean variance extraction (AVE) ranged from 0.517 to 0.719 and Cronbach’s α value ranged from 0.757 to 0.911. As a result, the convergence validity was confirmed to be significant.

Table 4. Results of reliability and convergent validity test.

Table 4. Results of reliability and convergent validity test.

The goodness-of-fit analysis of the structural equation model revealed a χ² of 398.021. The Comparative Fit Index (CFI) value was 0.920, and the Tucker-Lewis Index (TLI) value was 0.911, both of which were significant at levels above 0.9. The Root-Mean-Square Error of Approximation (RMSEA) value of 0.036 and the Standardized Root-Mean-Square Residual (SRMR) value of 0.031, both of which were significant below 0.1, indicated that the measurement model fit the constructs statistically significantly (see Table 5).

Table 5. Goodness-of-fit of confirmatory factor analysis.

Table 5. Goodness-of-fit of confirmatory factor analysis.

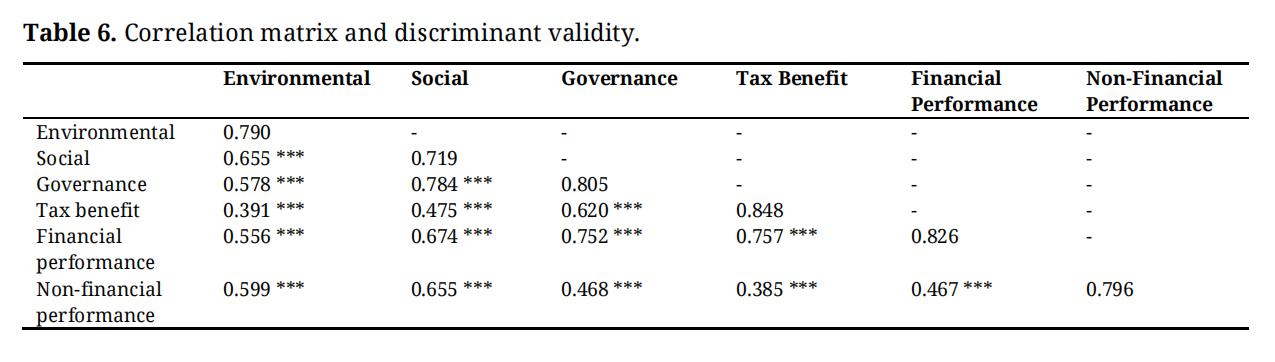

Pearson correlation analysis was used to determine the degree of correlation between variables. The square of the correlation coefficient for each variable was also calculated to evaluate the discriminant validity. As a result of statistical analysis, as shown in Table 6, all factors showed significant correlations.

Table 6. Correlation matrix and discriminant validity.

Table 6. Correlation matrix and discriminant validity.

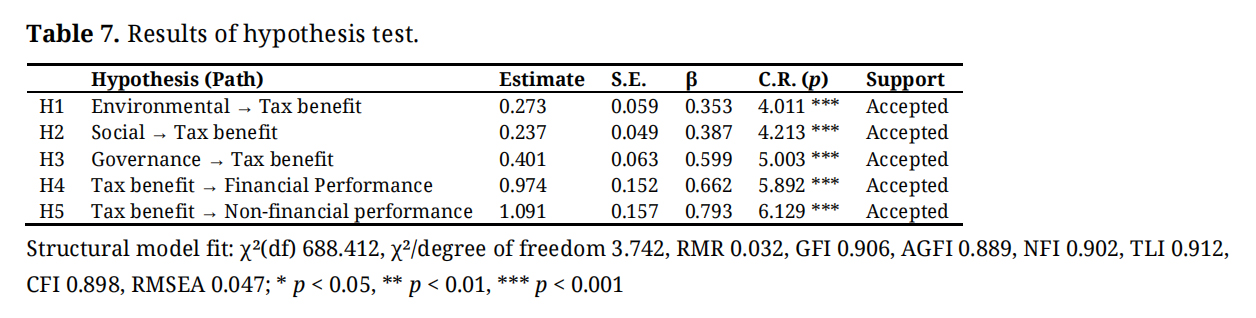

The goodness-of-fit of the structural model was analyzed (see Table 7), and the resulting χ² (df) value was 688.412, with a corresponding χ² degree-of-freedom value of 3.742. The model demonstrated satisfactory performance, with a Goodness-of-Fit Index (GFI) of 0.906 and a Normal Fit Index (NFI) of 0.902. The Root-Mean-Square Residual (RMR) was 0.032, the Adjusted Goodness-of-Fit Index (AGFI) was 0.889, and the RMSEA was 0.047, indicating that the model’s goodness-of-fit was significant. The CFI, which indicates the explanatory power of the model without being affected by the sample, was 0.898, and the TLI, which determines the explanatory power of the structural model, was 0.121. These values indicate that the basic model was a good fit. Hypothesis testing was conducted through path analysis of the structural equation model, which resulted in the acceptance of the five hypotheses. ESG Environmental had a positive effect on tax benefits (4.011, p < 0.001) and ESG Social Contribution had a positive effect on tax benefits (4.213, p < 0.001) and ESG Governance had a positive effect on tax benefits (5.003, p < 0.001). Tax benefits had a positive effect on financial corporate performance (5.892, p < 0.001) and non-financial performance (6.129, p < 0.001).

In addition, the bootstrapping method was used to evaluate the significance of indirect effects. As a result, ESG management and tax benefits were found to have direct and indirect mediating effects. This indicates that ESG management and tax benefits affect corporate performance through direct and indirect mediating effects, and all of these factors have positive effects.

Table 7. Results of hypothesis test.

Table 7. Results of hypothesis test.

This study empirically investigated the impact of ESG management on tax benefits and corporate performance. This analysis led to the following key findings: First, ESG management has a positive (+) effect on financial and non-financial corporate performance through the mediating effect of tax incentives. These results indicate that a prior study [8–12]. Chelawat et al. [62] argued that ESG management not only improves operational efficiency and financial performance, but also maximizes short-term and long-term financial performance through tax incentives. Therefore, the results of this study confirmed that tax incentives related to ESG management activities positively affect a company’s financial performance, as suggested in previous studies by Ivus et al. [53], Mamman et al. [63]. Effective tax credit and exemption policies, such as tax credits, tax refunds, and the provision of direct and indirect financial subsidies to companies, can greatly increase a company’s resilience to risk. These results suggest that these factors can also act as important drivers in the context of ESG management. Tax benefits derived from ESG management not only lead to direct tax savings, but also contribute to improving financial performance by minimizing capital costs, increasing investment attractiveness, and strengthening risk management.

Therefore, ESG management activities can increase net income and improve profitability indicators such as ROE and ROA by minimizing the corporate tax burden through benefits such as tax credits, exemptions, and deduction costs. In particular, investment tax credits for eco-friendly facilities and job-creating companies can have a positive impact on a company’s financial statements. From the perspective of tax incentives, we have indirectly confirmed that ESG management can have a positive impact on a company’s financial performance. These effects include increasing net income, improving profitability indicators, strengthening reinvestment capabilities through cash flows, enhancing financial stability, and minimizing capital costs such as falling interest rates and stock prices. ESG management also shows that it can contribute to mitigating tax regulatory risks, increasing the attractiveness of ESG-related investments, and ultimately promoting long-term corporate value growth.

Second, it was found that tax benefits also affect the non-financial performance of companies in the context of ESG management. These findings are consistent with those of Dhaliwal et al. [64], who explained that they positively affect stakeholder trust and corporate reputation. Non-financial performance refers to factors that are not directly reflected in the financial statements, such as stakeholder relationships, corporate image, sustainability, and employee satisfaction, but have a significant long-term impact on corporate value. Ultimately, ESG management, which encompasses non-financial factors such as environmental initiatives, social responsibility, improved governance, and relationships with employees, customers, and suppliers, can act as an important asset in determining future price competitiveness and profitability and have a positive impact on long-term management value growth.

Tax benefits from ESG management activities are officially recognized for their excellence in these areas, as they are given as a result of efforts to protect the environment, social responsibility, and improve governance. Furthermore, they can have a positive impact on increasing the evaluation of a company’s ethics, responsibility, and transparency from external stakeholders such as customers, partners, and government agencies. They also can lead to continued long-term customer loyalty, expanded partnerships, and expanded opportunities for policy benefits.

Nowadays, companies focus on ESG management by taking the lead in environmental protection efforts such as resource conservation, promoting recycling, and protecting water resources. They also engage in social contributions including supporting vulnerable groups, fostering a workplace culture of gender equality, improving working environments, and considering social safety. Through these activities, ethical management practices such as regulatory compliance and transparent business operations are upheld, with the ultimate goal of achieving sustainable growth [65]. Adopting sustainable business practices means that companies must enhance their long-term value by considering not only financial performance but also non-financial activities such as environmental protection, social contributions, and ethical management. Those companies focus on sustainable tax strategies that are maintainable in the long term, rather than merely minimizing taxes in the short term [18].

However, most previous studies examining the factors that determine a company’s tax burden or tax strategy have focused on financial factors such as firm size, debt ratio, and financial performance, primarily from a short-term perspective centered on tax minimization, such as tax avoidance [66,67]. There are many previous studies on ESG management and tax benefits primarily focused on governance factors. However, this study has academic significance in that it deals with the three ESG factors—ESG—as part of ESG management, structurally examines and empirically tests the relationship between tax benefits and corporate performance. It empirically verified the relationship between ESG management and tax benefits and financial and non-financial corporate performance. The results of this study also present three practical implications.

First, the impact of corporate ESG management on tax benefits is becoming increasingly important, and its influence continues to grow in response to changes in government policies, institutional frameworks, and societal expectations. ESG management is a strategic approach through which companies go beyond mere earing profit to pursue environmental protection, social responsibility, and transparent governance. Governments should utilize tax policy as a benefit to promote such sustainable management practices. Currently, many worldwide countries are implementing tax benefits for environmental initiatives, such as allowing the deduction of carbon credit purchase costs and providing investment tax credits for renewable energy facilities, to promote carbon reduction and eco-friendly investments. In relation to social contribution, various tax benefits are being implemented, including those for employing vulnerable groups such as persons with disabilities, the elderly, and young people in regular positions, as well as for corporate social responsibility activities and donations to public-interest foundations. In relation to corporate governance, tax benefits and preferential treatment in tax audits are provided when companies establish transparent accounting practices and effective internal control systems. Ultimately, companies should move beyond merely pursuing the value of sustainable management through ESG practices and develop internal tax strategies to maximize the tax benefits associated with ESG management, thereby creating synergies that enhance corporate performance.

Second, ESG management activities enhance trust from consumers, investors, and local communities, thereby strengthening brand loyalty and reputation in the market. From an organizational perspective, the integration of ESG management creates a more desirable working environment, promotes diversity and inclusion, and reinforces ethical governance. These developments align with the purposes of government tax benefit policies designed to encourage ideal corporate governance. Consequently, this alignment contributes not only to the fulfillment of public policy goals but also to internal organizational benefits, including reduced employee turnover, increased job engagement, and the enhancement of employees’ social responsibility. As a result, it aligns with the government’s strategies to advance corporate social responsibility activities. Specifically, tax credits for charitable donations and benefits for hiring vulnerable groups serve to promote the fulfillment of social responsibilities, thereby contributing to the enhancement of corporate social value. Therefore, corporations should not perceive ESG-related tax benefits merely as simple tax deductions, but rather as strategic tools to strengthen social trust, build a sustainable management culture, and enhance long-term corporate resilience and competitiveness. These benefits should be leveraged as non-financial assets that contribute to sustainable value creation.

Research Limitations and Future PlansThe findings and implications of this study contribute to enhancing corporate tax leaders’ understanding of ESG management and provide more specific insights into tax benefits and ESG management improvements for corporate performance. Nevertheless, this study has the following limitations: The first limitation includes the specificity of the sample and the limitations of generalization. Since this study was conducted on tax leaders and management of Korean companies, there is a limit to generalizing the results to other countries or industries. There may be differences in national and organizational culture because each country’s economic, cultural, social, and legal environment is different. In addition, the perception of corporate managers and tax leaders may vary depending on the size and type of organization. Research is needed that considers these differences.

Second, this study does not provide insight into how ESG management and tax benefits may vary depending on the type of company. ESG management differs according to the industry and company type, and tax benefits vary according to the type of company and industry. Considering these points, a comparative study considering the type of company, type of industry, and differences in tax benefits should be conducted empirically.

Third, this study uses ESG management as a major variable, but further analysis is needed on the practical factors that ESG management affects corporate performance, especially in relation to tax benefits. Therefore, in future studies, qualitative methods such as interviews and case studies need to be used to discover ESG management impact variables related to tax benefits and conduct more specialized research related to tax benefits.

The survey was agreed upon by the participants, the study was conducted according to the General Data Protection Regulation (Regulation No. 2016/679) of South Korea. Data are not publicly available due to the privacy of respondents.

Conceptualization, EL; methodology, EL; software, EL; validation, EL and BK; formal analysis, BK; investigation, EL and BK; resources, EL and BK; data curation, BK; writing—original draft preparation, EL and BK; writing—review and editing, BK; visualization, BK; supervision, BK; project administration, BK; funding acquisition, EL.

The authors declare no conflicts of interest.

This paper is written with support for research funding from aSSIST University.

1.

2.

3.

4.

5.

6.

7.

8.

9.

10.

11.

12.

13.

14.

15.

16.

17.

18.

19.

20.

21.

22.

23.

24.

25.

26.

27.

28.

29.

30.

31.

32.

33.

34.

35.

36.

37.

38.

39.

40.

41.

42.

43.

44.

45.

46.

47.

48.

49.

50.

51.

52.

53.

54.

55.

56.

57.

58.

59.

60.

61.

62.

63.

64.

65.

66.

67.

Lee E, Kim, B. The effect of corporate ESG management on tax benefits and corporate performance—Findings from South Korea. J Sustain Res. 2025;7(4):e250063. https://doi.org/10.20900/jsr20250063.

Copyright © Hapres Co., Ltd. Privacy Policy | Terms and Conditions